How Much Does a House Valuation Cost?

TL;DR: In London, a proper RICS house valuation or survey-based valuation typically costs from £400 to over £1,000, depending on the property’s size, value and complexity. A cheap lender valuation or desktop figure isn’t the same thing and often won’t tell you what you need to know.

You’re probably seeing three different numbers already. The estate agent has one. The lender has another. An online calculator has a third. That’s normal, and it’s exactly why people ask, how much does a house valuation cost and why the answers seem all over the place.

The short answer is this. You need to know what sort of valuation you’re paying for, who it’s for and what job it’s meant to do. In London, that difference matters even more because a Victorian terrace in Forest Hill, a flat conversion in Peckham and a modern flat in Stratford are not remotely the same proposition.

Table of Contents

- Understanding the Real Cost of a House Valuation

- Mortgage Valuations vs Market Valuations What's the Difference

- Key Factors That Determine Your Valuation Fee

- What You Get for Your Money a RICS Valuation Breakdown

- How to Get an Accurate Quote and Avoid Overpaying

- Frequently Asked Questions About House Valuation Costs

Understanding the Real Cost of a House Valuation

Most confusion starts with the word valuation itself. Estate agents use it to win an instruction. Lenders use it to protect their loan book. Online tools spit out a rough estimate based on past data. None of those is the same as an independent RICS valuation.

A proper valuation is an expert opinion of market value prepared for a defined purpose. That purpose might be a purchase, probate, matrimonial proceedings, Capital Gains Tax or a shared ownership staircasing matter. If the report may be relied on financially or legally, it needs to be done properly.

That’s why the fee isn’t just for a number at the bottom of the page. You’re paying for inspection, local market evidence, professional judgement and accountability under RICS rules.

Practical rule: If the valuation may end up in front of a solicitor, lender, HMRC or a court, don’t rely on an agent’s estimate or an online calculator.

For probate work, accountants and executors also need to understand the tax side of the process, not just the property figure. A useful plain-English primer is this guide to Estate valuation for IHT purposes, which helps explain why the basis of valuation matters.

If you want the wider map of what each type of valuation is for, this Corinthian guide on property valuations in London every type explained and when you need one is worth reading before you instruct anyone.

Mortgage Valuations vs Market Valuations What's the Difference

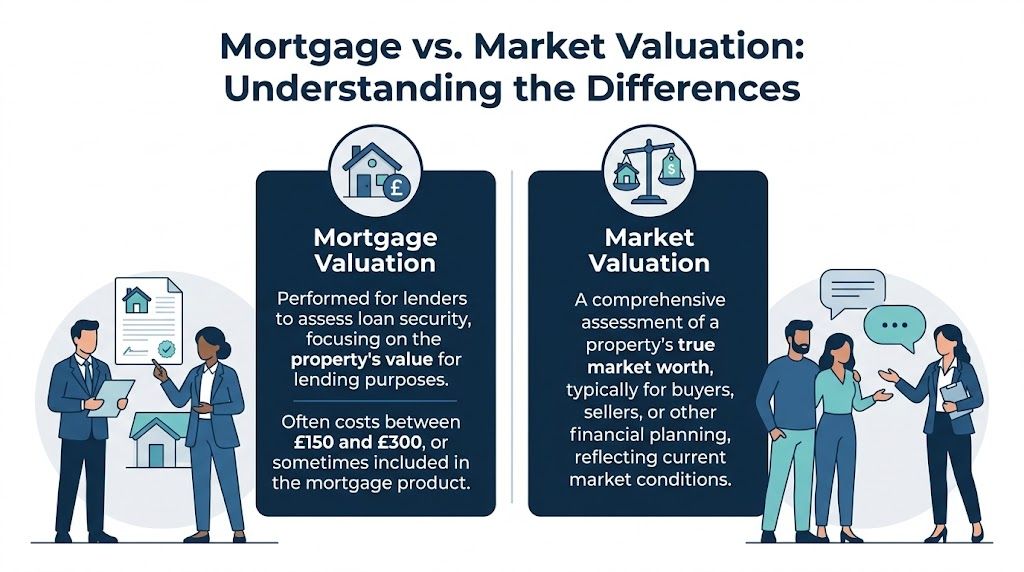

The biggest mistake I see is people assuming the lender’s valuation protects them. It doesn’t. It protects the lender.

Here’s the visual version first.

Who the valuation is really for

A mortgage valuation is a lending check. The lender wants to know whether the property gives adequate security for the mortgage. It may be brief. It may be desktop only. It may involve little or no attention to defects that would matter greatly to you as a buyer.

A market valuation, by contrast, is for you or for a defined formal purpose. It is meant to stand up as a reasoned opinion of value, not a quick lending filter.

Cheap options exist, but they come with limits. Free or low-cost Automated Valuation Models or lender Drive-By Valuations often cost £0-£200 and miss critical defects, while RICS Level 2 HomeBuyer Reports cost £500-£800 for London properties under 100sqm and can uncover issues leading to price reductions of up to 20% (Bankrate).

That gap matters in London. A flat in Bermondsey with leasehold complications, a damp-prone terrace in Brockley or a maisonette in Sydenham with movement cracks can all look acceptable from the outside.

Later in the process, many buyers realise they needed a survey-based valuation, not a lender tick-box exercise. That’s avoidable.

A simple side by side comparison

| Valuation type | Main purpose | Who it serves | Inspection depth | Typical cost |

|---|---|---|---|---|

| Mortgage valuation | Loan security check | Lender | Usually limited | Often low cost or included by lender |

| AVM or drive-by | Quick estimate | Lender or buyer seeking a rough figure | Very limited or no internal inspection | £0-£200 |

| RICS HomeBuyer Report with valuation | Purchase advice plus value opinion | Buyer | Internal inspection with condition ratings | £500-£800 for many London homes under 100sqm |

| RICS market valuation or formal Red Book valuation | Market value for a defined purpose | Client, solicitor, court or HMRC depending on instruction | Proper inspection and evidence-based analysis | Usually higher because it carries formal responsibility |

If you want a broader read on how valuers approach the job itself, this piece on mastering real estate property valuation methods is a useful backgrounder. Just don’t confuse the theory with what’s needed for a formal UK residential instruction.

A lender valuation answers one question: is the property adequate security for the loan. A proper valuation answers the question you actually asked.

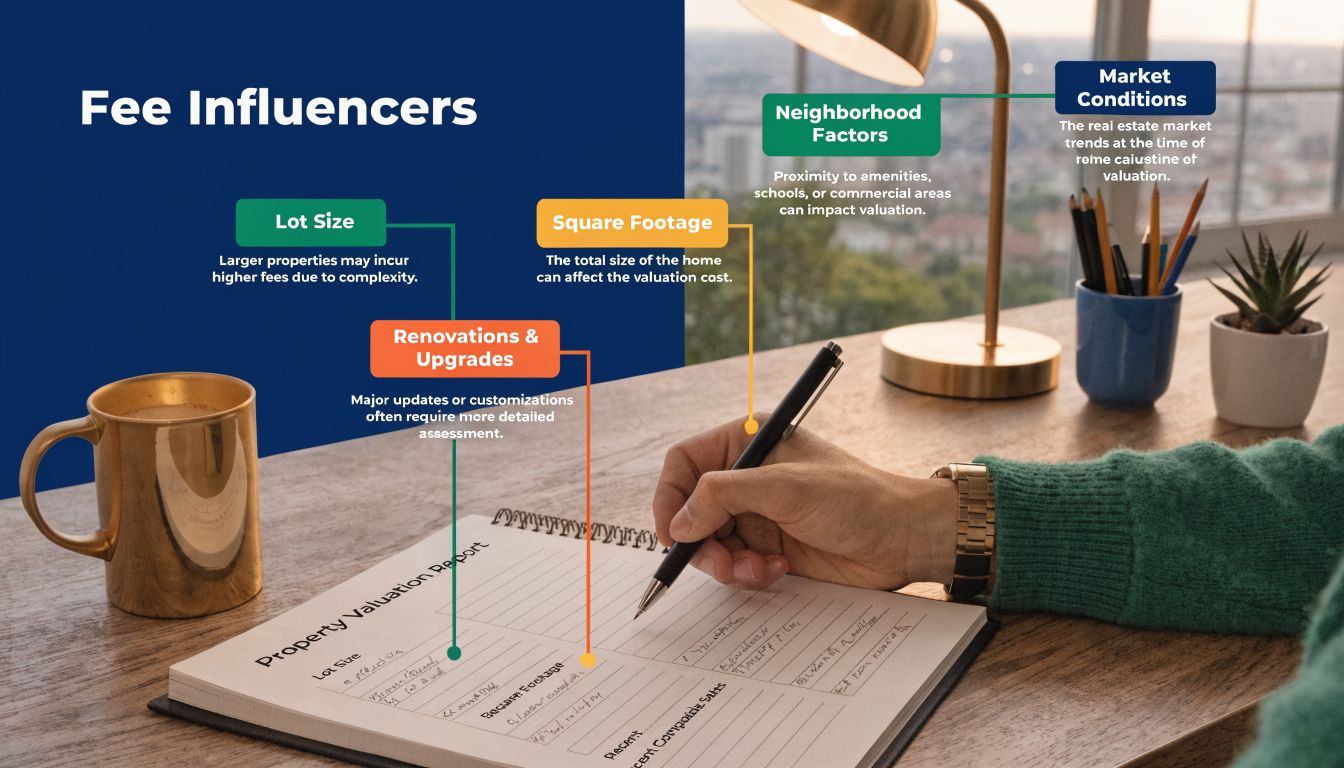

Key Factors That Determine Your Valuation Fee

In London, the fee follows the job. A quick lender valuation is one thing. A proper RICS market valuation for a buyer, seller, probate matter or legal dispute is another, and it costs more because the surveyor is doing more and carrying more responsibility.

The property itself drives the fee

Start with the property, because that is what sets the workload.

A small modern flat in a block with plenty of recent comparable sales is usually straightforward to value. A large Victorian house in Wandsworth, a converted property in Hackney, or a period terrace in Lewisham with alterations and patchy paperwork is not. The inspection takes longer. The analysis takes longer. The risk to the surveyor is higher.

The main cost drivers are usually:

- Size: More floor area means more to inspect, assess and compare.

- Age and condition: Older London stock tends to hide more defects and alterations.

- Construction type: Standard homes are simpler than listed buildings, non-standard construction, basements, roof terraces or heavily extended houses.

- Tenure and legal complexity: Leasehold flats, short leases, share of freehold arrangements and unusual titles often need closer attention.

- Comparable evidence: Some postcodes give you clear local evidence. Unique homes do not.

That is why two properties worth broadly similar amounts can attract different fees. The value matters, but the complexity matters just as much.

The purpose of the valuation changes the price

This catches people out all the time.

If you only need a rough figure for your lender’s file, the job is limited. If you need a defensible market valuation for a sale decision, probate, tax, matrimonial proceedings or a dispute, the surveyor has to inspect properly, analyse the evidence and stand behind the opinion in writing.

That wider scope pushes the fee up. So does the level of reporting. A formal valuation for legal or tax purposes is not priced like a quick opinion for mortgage processing.

HomeOwners Alliance notes that many buyers underestimate the value of a proper survey and valuation until defects come to light (HomeOwners Alliance). In London, where one issue with structure, lease terms or alterations can shift value sharply, paying for the right instruction at the start is the sensible move.

My advice is simple. If the property is older, unusual, extended, converted, or tied to a legal process, do not shop for the cheapest quote. Get the right valuation for the purpose. That is the fee that saves money.

What You Get for Your Money a RICS Valuation Breakdown

A proper RICS valuation is not a one-line figure. It’s a reasoned report built from inspection and evidence.

What goes into the report

A RICS HomeBuyer Report integrates a condition rating and market value estimate derived from comparable sales analysis within a 0.5-mile radius, adjusted for condition under the Red Book. These reports can uncover defects such as subsidence, which affects 1 in 50 London properties (NHBC).

That means the process usually includes:

- An on-site inspection: The surveyor looks at the property as it exists, not as the brochure describes it.

- Comparable evidence: Recent nearby sales are reviewed and adjusted for size, condition and other differences.

- Condition context: Value isn’t looked at in isolation. Defects can affect what a buyer should pay.

- A written report: This gives a clear record of the figure and the reasoning behind it.

For buyers who are unsure which report level they need, this guide to RICS survey levels explained which one do you actually need is useful because it separates Level 2 from Level 3 without the usual waffle.

Why independence matters

For legal or financial purposes, the valuer must be independent and properly regulated. That’s the point. If the person giving the figure is also trying to sell the property, win the mortgage business or keep a developer happy, you’ve got a conflict before you’ve even started.

Corinthian Surveyors London LTD is one example of the sort of practice people should look for in this situation: independent, RICS regulated, in the Valuers Registration Scheme and led by a surveyor with RICS and CABE qualifications. That matters more than glossy branding.

The value of the report is in the reasoning, the inspection and the fact that the surveyor stands behind it.

How to Get an Accurate Quote and Avoid Overpaying

You call three firms for a valuation on a flat in London. One says £350, one says £750, and one says, "It depends." The cheapest quote often leaves out the very points that make London property difficult, especially lease length, alterations, access, and the actual purpose of the report.

Start by giving the surveyor enough detail to price the job properly. If you want a direct fee based on the property itself, not a guessed figure, say exactly what the property is and what the valuation needs to do.

What to have ready before you ask for a fee

Have these details ready:

- The full address: Postcode matters in London because value can shift street by street.

- Property type: Flat, terrace, semi, conversion, listed building, ex-local authority, or new build.

- Approximate age: Victorian, Edwardian, interwar, post-war, or modern.

- Purpose of the valuation: Purchase, sale, probate, tax, matrimonial, Help to Buy, or another legal purpose.

- Any known issues: Cracks, damp, short lease, non-standard construction, basement excavation nearby, loft conversion, or altered layout.

Be straight about defects and complications. If a flat has a short lease or a house has movement, say so at the start. That helps the surveyor quote for the right instruction instead of giving you a low headline price that rises later.

How to avoid paying for the wrong thing

First, make sure you are asking for the right service.

A lender's valuation is for the bank. It is not the same as a proper RICS market valuation for you, and it will not replace a report needed for probate, tax, court, or a reasoned buying or selling decision. In London, that distinction matters because unusual layouts, conversions, leasehold problems, and mixed-condition stock are common.

If you are buying and already need a survey, ask whether a valuation can be added to the survey instruction. That is often the most sensible route on a standard purchase. If the property is older, heavily altered, or legally sensitive, pay for the correct report from the start. A cheap, light-touch option usually costs more once you have to order the proper valuation afterwards.

Ask four direct questions before you instruct:

- Is this a formal RICS valuation or just an estimate?

- Is the fee fixed?

- What assumptions are you making about lease length, title, condition, or access?

- Will the report be suitable for my purpose?

If the answers are woolly, move on.

Choose an independent RICS surveyor with no tie to the estate agent, lender, or developer. That reduces the risk of a superficial figure dressed up as advice. Corinthian Surveyors London LTD provides this type of instruction. A proper market valuation, prepared for the stated purpose and based on the actual property, is what you should be paying for.

If you want a direct fee based on the actual property rather than a generic estimate, ring 0800 00 16 422 with the address and the purpose of the instruction.

Frequently Asked Questions About House Valuation Costs

A few points come up again and again, especially in London where probate, leasehold and older housing stock complicate matters.

RICS valuation fees in London have risen 8% year on year due to a 12% surveyor shortage and post-2025 regulatory hikes, and probate valuations now average £600-£1,200, up from £500, because compliant reports are required for HMRC (Law Society).

That explains why fees feel firmer than they did a few years ago. It isn’t arbitrary. There’s more regulation, more demand and not enough qualified surveyors.

If you want more general answers on report types and process, Corinthian also has a useful FAQs page.

| Question | Answer |

|---|---|

| Is a lender valuation enough when I’m buying? | No, not if you want advice for yourself. A lender valuation is for the lender. If you need a reasoned view of condition and value, instruct a proper RICS survey or valuation. |

| Why does London cost more? | Because the property stock is more varied, values are higher and unusual issues are common. Victorian conversions, short leases, altered layouts and defect risk all add work. |

| Do I need a formal valuation for probate? | Usually yes, if the figure needs to stand up for HMRC and estate administration. A casual estimate isn’t the same thing. |

| Is an online valuation any use? | It can be a starting point only. It won’t inspect the property and it won’t account properly for defects, alterations or legal quirks. |

One last point. Don’t shop for this service the way you’d shop for boiler insurance. The cheapest figure often buys the least useful report.

If the property is in Forest Hill, Blackheath, Peckham, Bromley, Balham or anywhere else in London, the right fee is the one that gets you the right level of professional judgement for that specific building and that specific purpose.

If you need a formal residential valuation or survey-based valuation in London, Corinthian Surveyors London LTD handles market valuations, probate work and RICS survey instructions across the capital. The sensible next step is to provide the address, property type and purpose of the report so the quote matches the job rather than guessing from a headline price.